Introduction

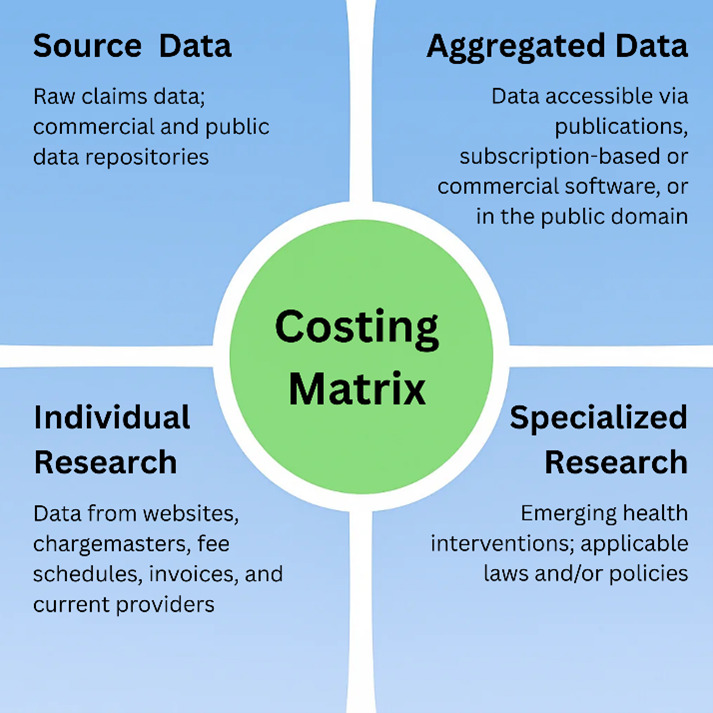

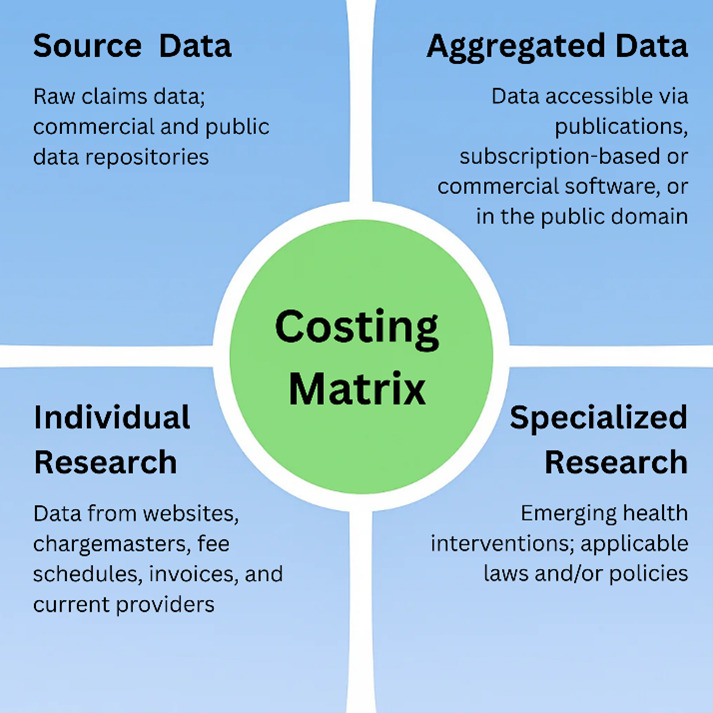

As healthcare pricing approaches are becoming increasingly complex, life care planners need guidance in the life care planning costing process. This chapter introduces a life care plan costing matrix that identifies four primary types of costing data referenced in life care planning: source data, aggregated data, individual research, and specialized research. The sections that follow provide a detailed overview of each category of data, along with a visual summary of the costing matrix (see Figure 1) to aid implementation.

Methodology

The Costing Framework working group decided at the meeting on February 22, 2023 to form a subcommittee to define costing categories and to develop a graphic to educate life care planners. The subcommittee first convened on March 8, 2023 with 10 members and discussed its scope of work, key deliverables, and group consensus process. It was determined that at least 80% of subcommittee members needed to agree on decisions by vote. Over the course of the project, the subcommittee held a total of 14 meetings dedicated to developing a classification system for costing data through collaborative deliberation. Two subcommittee members discontinued participation. The subcommittee ultimately devised a costing matrix to systematize and contextualize costing approaches, along with a definition of each costing category and considerations for life care planners.

Results

The analytical phase of the subcommittee’s work led to the identification of four primary types of cost sources: source data, aggregated data, individual research, and specialized research. One hundred percent of the subcommittee agreed on these four categories of costing data. It was further agreed that a costing matrix was the most appropriate way to conceptualize the categories. The costing matrix organizes healthcare cost information into four distinct quadrants based on two key dimensions: data granularity (source versus aggregated) and research scope (individual versus specialized). (See Figure 1 below.) The life care planner is responsible for selecting the type of data chosen in the development of each life care plan, and more than one data source may be used in a life care plan. To aid in the selection process, a discussion of each category of data is presented below the figure.

Source Data

Source data refers to raw claims data from commercial insurers and public repositories. It is unprocessed, detailed transactional data that serves as the foundation for cost analysis. It represents the most granular level of data. All source data discussed in this project originates from charges submitted by healthcare providers through standardized claim forms that comply with federally mandated HIPAA transaction code sets. Specifically, the data are derived from facility (institutional) claim forms such as the UB-04, also known as CMS-1450 (National Uniform Billing Committee, n.d.), and professional claim forms, known as the CMS-1500 (National Uniform Claim Committee, n.d.). These standardized electronic transaction forms adhere to HIPAA Administrative Simplification provisions in the United States (Health Insurance Portability and Accountability Act of 1996) and gather billing information related to medical procedures, services, and diagnoses for submission to government and private payers, either directly or via clearinghouses.

Source data are then electronically processed by government agencies, insurance companies, and third-party organizations in file formats known as 837i, used by hospitals and other institutional providers (Centers for Medicare & Medicaid Services [CMS], n.d.-a), and 837p, used by healthcare professionals (CMS, n.d.-b). Raw data are collected from 837p and 837i claim files formatted in standardized CMS layouts, including fields such as procedure codes, charges, and revenue codes. 837i files typically do not include data from self-paying patients, cash-only providers, or property and casualty claims (e.g. motor vehicle accidents). When this chapter references CMS claim forms, it refers to the standardized forms required under HIPAA transaction code sets, not to CMS policy or reimbursement guidelines.

Once the data are processed, they are accessed and compiled through various channels, including governmental repositories, private sector sources, and commercial software platforms that aggregate, reformat, and sometimes license the data for external use. Large database aggregators may not include claims data from property and casualty claims or providers who choose not to accept insurance.

Life Care Planning Considerations

Many primary-source data collections in government files are accessible to the public. In the United States, these may include state agency or federal files, such as those from the CMS. Data in the public sector are aggregated from claim forms, e.g., professional and facility claim forms, and private-sector data are aggregated from patient forms and claims data. Charge databases include both private-sector and public-sector charge data. This will be discussed further in the aggregated data section of this chapter. Life care planners should use clinical judgment if they are using claims data from databases, as the data are aggregated and are not segregated by provider specialty, license type, health condition, etc., which may affect the cost of a good or service.

Each country has their respective private and government claims data collection processes. Within the costing matrix, any use of governmentally sourced data should be made within the regulatory framework of the country where the evaluee lives or receives care and be presented in accordance with that country’s coding standards.

Aggregated Data

For purposes of this project, aggregated data refers to source data that has been processed, compiled, or converted into formatted reports, summaries, or retrieval tools for analysis or life care plan costing analysis. Source data is the foundation for aggregated data. Once the data have been combined, they can no longer be identified with any individual (U.S. Department of the Treasury, n.d.). The processed data, or aggregated data, can be found in publications, subscription-based or commercial software, or public domains that provide access to data abstracted from processed raw claims. These data are grouped by diagnosis and procedure codes used by prospective payment systems, and they are used by health care organizations, policymakers, and researchers to inform decision-making and set payment rates, among other activities.

To ensure uniformity, standardization, and reliability, electronic health claims data movement must follow HIPAA Transaction Code Sets in the United States. The uniformity of the aggregated data by federal definition and billing practice standards ensures the data are reliable. Aggregated healthcare data originates from the legislated electronic claims submission process established by federal regulation. The HIPAA Transaction Code Sets, mandated by the Health Insurance Portability and Accountability Act of 1996, created standardized formats for electronic healthcare transactions (Department of Health and Human Services [HHS], 2000). This legislation, specifically through Sections 261-264 and the addition of Section 1173 to the Social Security Act, required HHS to develop and implement national standards for electronic healthcare transactions, code sets, unique identifiers, and security measures (HHS, 2017). Following the October 16, 2003 compliance deadline, healthcare providers began submitting claims in these standardized formats, enabling data aggregators to collect this information for purposes beyond payment processing (CMS, 2017). This standardization and uniformity have revolutionized healthcare data analytics by establishing consistent, reliable data sources that support sophisticated analytical applications and enhance decision-making capabilities across the healthcare ecosystem (HHS, 2024).

Life Care Planning Considerations

Aggregated claims data are used heavily in various types of research. Such aggregates are used by providers, payors, and various governmental agencies. Healthcare organizations, insurers, and government agencies regularly analyze these data collections to inform decisions and policy. Life care planners also rely on these aggregated repositories when determining appropriate costs for services and products in life care plan recommendations. Aggregated data provide a consistent basis for providing a reasonable charge for services and products recommended in a life care plan. The use of non-collateral (i.e., non-contractual or non-discounted) aggregated data is consistent with Consensus and Majority Statement #85 (Johnson et al., 2018, p. 17, 2025, pp. 72–3) and life care planning standards of practice (See Chapter 1).

Individual Research

Individual research is the process of collecting non-aggregated data to identify costs. It involves direct outreach using telephone calls, emails and letters to secure cost estimates, consultations with service providers, and independent market research. It encompasses costs for recommended services in a life care plan such as medical and surgical procedures, rehabilitation interventions, specialized products including orthotic devices, prosthetics, and adaptive equipment, home health care, transportation assistance, home modifications, and vocational rehabilitation. In addition to performing life care planning, the process of conducting individual research is part of the everyday clinical practice of rehabilitation counselors, case managers, nurses, and other qualified professionals who help identify costs for people seeking access to comprehensive medical care, supplies, and supportive and non-medical services.

Per the Hospital Price Transparency Rule effective January 1, 2021 (45 CFR Part 180), hospitals in the United States are required to post their standard chargemaster rates. It is the opinion of this subcommittee that hospital chargemasters constitute individual research and not aggregated data. While chargemasters represent compiled lists of institutional charges, for life care planning purposes, this can be considered individual-level research because the data contains specific, line-item charges at the institutional level. This is differentiated from aggregated data which cannot be identified by individual vendor.

Life Care Planning Considerations

Individual research is common among life care planners seeking to identify geographically specific costs of routine and unique care and procedures. Individual research is important to life care planners to also ensure the evaluee has access to medical care, supplies, and support within their geographic area and to define the costs associated with these services and items.

While many components of a life care plan are grounded in medical necessity and supported by standardized billing codes and pricing data, some essential services and supports fall outside the scope of traditional healthcare frameworks. Medical and non-medical items, including but not limited to aids for independent functioning, home furnishings, in-home services, facility-based care, transportation, and architectural modifications may not be associated with adequate procedure and supply codes or captured in medical charge databases, in which case individual research is needed. These efforts ensure that the life care plan reflects the full scope of an individual’s long-term needs, including those that are essential for functional independence and quality of life.

Specialized Research

An extension of individual research, specialized research addresses cutting-edge or policy-driven costing needs. Sources include cost-effectiveness studies reporting treatment costs, health economics research which provides cost comparisons, manufacturer data which includes the manufacturer’s suggested retail price (MSRP) or typical pricing, research reports, and clinical trials which document intervention costs. It is differentiated from individual research because it is not specific to a client or evaluee but relies on published information to provide foundational support for a life care plan.

Life Care Planning Considerations

Specialized research has been adopted in life care planning in response to the growing complexity of medical and non-medical interventions required for individuals with catastrophic injuries or rare conditions. This type of research is particularly useful when rare or uncommon services or products are needed by an evaluee. It supports the inclusion of emerging technologies, customized care strategies, and regionally variable services that cannot be costed through other methods. Specialized research requires in-depth analysis and consultation with unique informational sources. Examples could include custom-made durable medical equipment, robotic products, tailored environmental adjustments, and advances in health interventions. Additionally, there may be external factors that require specialized research to meet jurisdictional legal requirements related to costs included in a life care plan, such as application of collateral sources. The life care planner should be aware of jurisdictional requirements (See Chapter 3).

Discussion

The work of this subcommittee resulted in the identification of four primary categories of cost sources in life care planning: source data, aggregated data, individual research, and specialized research. The definition and life care planning considerations for each category were provided, and a costing matrix was created as a graphical representation of the four costing categories (see Figure 1).

Life care plan costing began as individual research and as healthcare pricing became more complex and technology advanced, databases emerged and have been adopted as a method of obtaining costs. However, acquisition of data through any of the four sources identified is useful and relevant. This chapter seeks to help life care planners understand the spectrum of data available and help life care planners to identify appropriate data sources based on their specific costing needs. As the field of life care planning evolves, new sources of costing research will emerge. The effectiveness of the Costing Framework largely depends on the clinical judgment of life care planners, who utilize their training, education, and experience to support the foundation for their opinions.

This Costing Framework aligns with the foundational teachings of Paul M. Deutsch, Ph.D., a pioneer in life care planning, who established that “At no time during the plan development process should budgetary concerns influence care and rehabilitation recommendations” (Deutsch & Reid, 2004, Chapter 5, p. 6). The development of this life care plan costing matrix represents an advancement in the understanding of life care planning cost research. It ensures that, as per Dr. Deutsch’s teachings, quality rehabilitation services remain broadly accessible.