When conducting costing research for a life care plan, it is essential to understand the primary goals of life care planning are to maximize an individual’s functional status following an injury or disability, prevent secondary complications, and promote overall quality of life. Life care plans are needs-based documents, derived from clinical evidence and functional assessment of the evaluee, rather than from limitations imposed by specific payors, insurance benefits, or collateral payment sources (Deutsch & Reid, 2004). A fundamental component of the life care planning process is the systematic determination of costs for the products and services recommended to address the evaluee’s identified medical, functional, and support needs.

At the 2022 Life Care Planning Summit, life care planners identified the need for a Costing Framework to clarify the variables and methods used in the costing process, along with the strengths and considerations when using those methods (Johnson et al., 2023). In response, a Costing Framework is presented in this chapter.

As described in Chapter 1, life care planners are guided by established Standards of Practice (International Academy of Life Care Planners [IALCP], 2022; American Association of Nurse Life Care Planners [AANLCP], 2015; American Academy of Physician Life Care Planners [AAPLCP], 2025) as well as Consensus and Majority Statements developed through biennial life care planning summits (Johnson et al., 2018, 2025) to ensure consistent, valid, and reliable approaches to obtaining life care plan costs. The Costing Framework is built upon this foundation as well as data regarding costing techniques gathered through the 2021 Costing Technique Survey (conducted as a precursor to the 2022 Life Care Planning Summit) and data obtained at the 2022 Summit. A consensus project defining primary cost sources, accompanied by an educational graphic, was presented in Chapter 4, and analysis of the data was provided in Chapters 5, 6, 7, and 8. This framework project offers a conceptual structure of common themes, costing techniques, and key considerations intended to support the life care planning cost research process. To further assist life care planners, a review of costing related resources was presented in Chapter 3. This information has also been integrated into the Costing Framework.

Guided by their education, training, and experience, life care planners apply clinical judgment (Choppa et al., 2004) that requires flexibility, as cost research methods may vary across situations. The Costing Framework was not designed to be prescriptive, but rather to serve as a tool that synthesizes data to identify commonly used costing techniques to provide education and guidance to life care planners. The goals of this project included identifying variables to be considered in cost-related decisions; recognizing circumstances in which variables are relevant; identifying common costing techniques; discussing considerations including strengths and challenges associated with various costing techniques; defining key terms; providing guidance for life care planning cost decisions; and assisting life care planners in supporting and defending their costing related decisions when utilizing various costing techniques.

Methodology

Following the 2022 Summit, committee co-chairs were selected to guide the Costing Framework Development Project. From July 18 to October 7, 2022, a call for volunteers was distributed via email to three life care planning associations, IALCP, AANLCP, and AAPLCP, for dissemination among their members. Leadership within AAPLCP declined participation in this project.

The Costing Framework Development Committee was initially formed with 55 volunteers, although due to attrition over time, 39 volunteers remained active throughout the project. Twenty-four volunteers served on the working group and 17 served on the advisory committee, including the two co-chairs, who served on both the working group and the advisory committee. Volunteers represented a diverse range of geographic locations, professional background, levels of experience, and professional credentials. Additional details regarding the development of the Costing Framework Development Committee and its processes are provided in Chapter 2.

The 2021 Costing Technique Survey Subcommittee, Top Hat Data Subcommittee, and Summit Notes and Summit Recording Subcommittee analyzed their respective data and identified common themes, costing techniques, and considerations associated with the use of various costing techniques. The findings are reported in Chapters 6, 7, and 8, and were considered, alongside the published quantitative analysis presented in Johnson et al. (2023), as reported in Chapter 5.

In Chapter 6, themes were synthesized and organized into six categories: standards of practice (SOP)/consensus statements; practice management; aggregated data; individual research; learning techniques; and problems encountered. Standards of practice and consensus statements refer to published guidelines that encourage life care planners to use data that are reliable, valid, and geographically representative. Practice management reflects the clinical judgment and individualized approaches life care planners use to research and document costs, often incorporating multiple costing sources. Aggregated data refers to cost information synthesized and compiled from multiple sources, where individual research refers to cost information obtained independently and not derived from aggregated sources. Learning techniques encompass the various methods life care planners use to develop and refine cost research skills. Problems encountered refers to considerations or challenges reported when using costing techniques. Responses identified as problems encountered (challenges) in Chapter 6 were later synthesized along with challenges reported in Chapters 5 and 7 to create a summary of challenges to be considered (See Table 3). Therefore, problems encountered, identified in Chapter 6, did not remain as a separate thematic category for this overall project.

Five thematic categories are represented in the Costing Framework to reflect current life care planning costing practices. Examples of reported strengths associated with these practices are also incorporated. The framework preserves the autonomy of the life care planner and ensures that practitioners retain discretion to select the costing processes and methodologies they determine to be most appropriate in support of their expert opinions.

Results

Four types of cost sources are detailed below, followed by considerations of strengths and challenges associated with the use of aggregated data and individual research costing techniques. Results illustrating the five thematic categories represented in the Costing Framework are also provided.

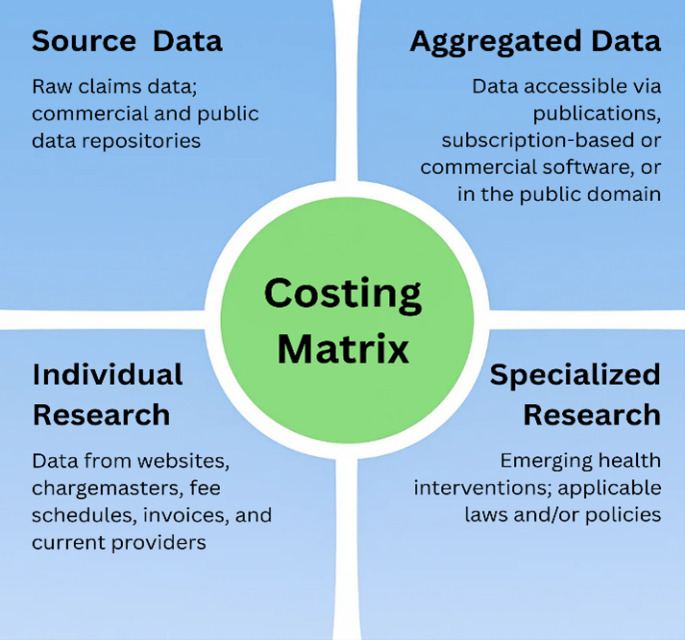

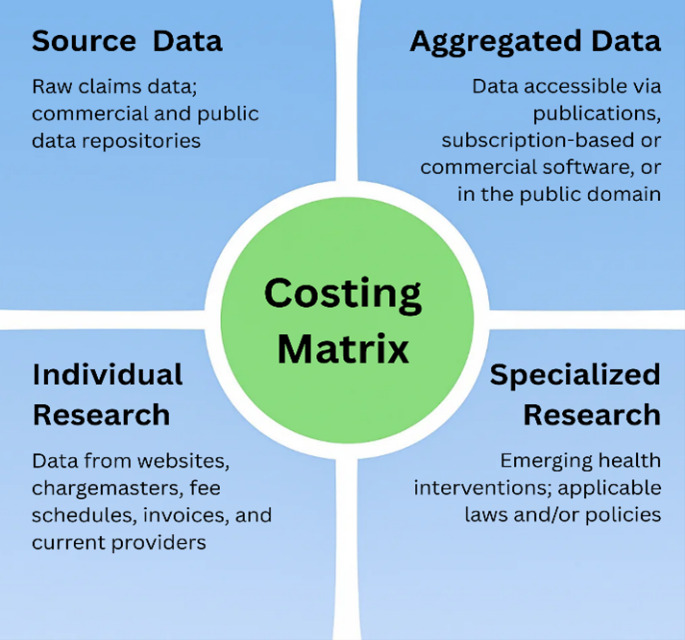

The Costing Matrix Subcommittee identified four types of costing sources, as represented in Table 1. Life care planners use clinical judgment to select the types of data chosen in the development of each life care plan, and more than one data source may be used. The Costing Matrix shown in Figure 1 was developed to organize these sources into four distinct quadrants and serve as an educational tool to explain the four costing sources.

The following tables summarize reported considerations as strengths and challenges that may influence life care planners’ individual costing research choices. This summary is based on responses presented from Chapters 5, 6, and 7 to provide considerations to assist life care planners in making informed decisions about costing techniques across varied situations. Life care planners use various databases; however, participants’ responses may not apply to all databases. Refer to Chapters 5, 6, and 7 for more detailed information.

Thematic Findings

During the development of this project, identified themes were synthesized and organized into five categories: standards of practice (SOP)/consensus and majority statements; practice management; aggregated data; individual research; and learning. The five categories were incorporated in the Costing Framework to reflect current life care planning costing practices. Tables 4 through 7 present a synthesis of data from the 2021 Costing Technique Survey quantitative results, 2021 Costing Technique Survey qualitative results, 2022 Summit Top Hat qualitative results, and 2022 Summit discussions, with findings grouped according to these five categories.

Costing Framework

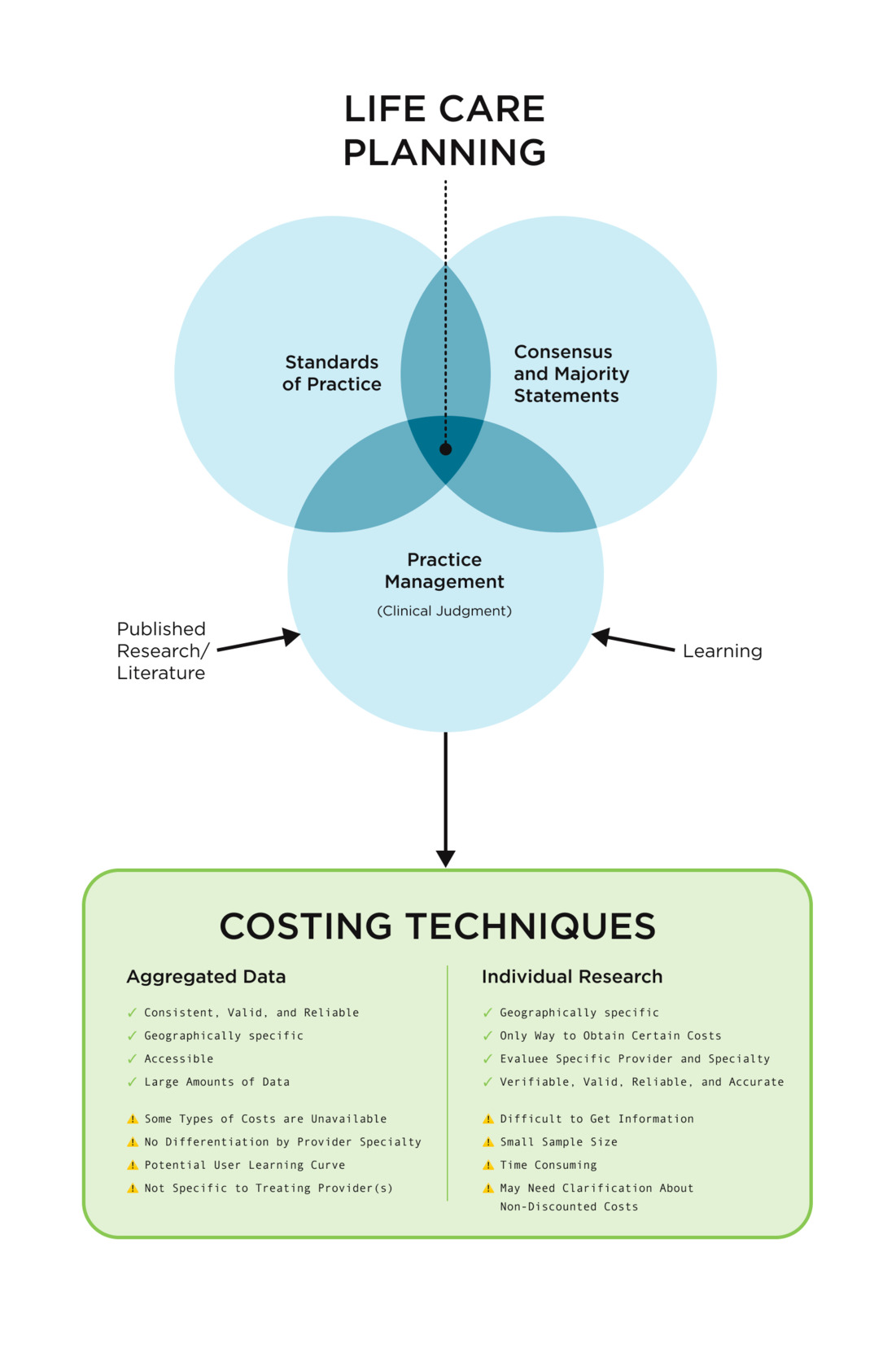

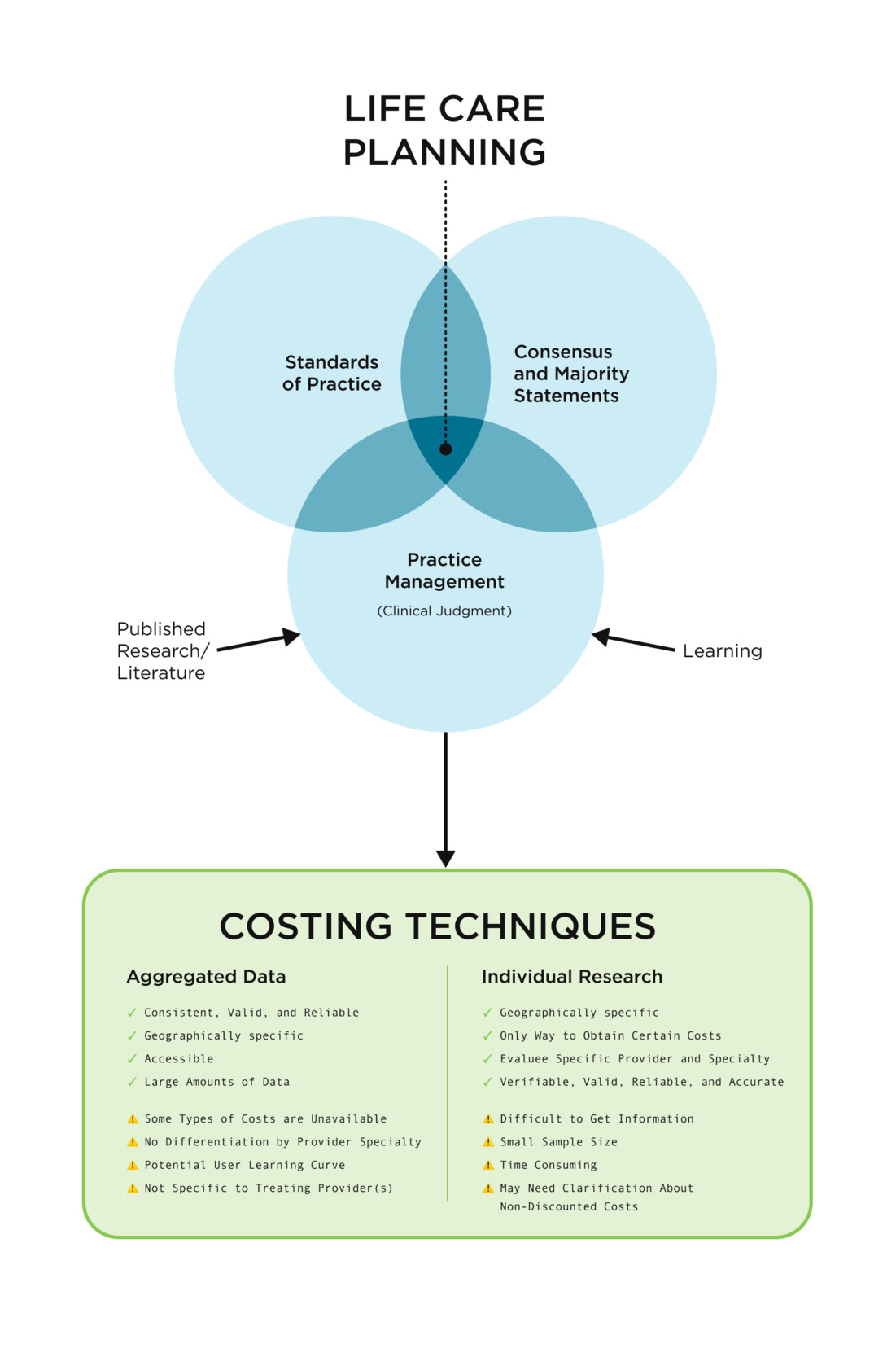

The Costing Framework presented in Figure 2 illustrates two commonly reported costing techniques used by life care planners and the five thematic categories that assist in the life care plan costing process. Further, it includes examples of considerations regarding strengths and challenges associated with each technique, derived from analysis of the data in Chapters 5, 6, 7, and 8.

The Costing Framework diagram presented in Figure 2 illustrates how standards of practice, consensus and majority statements, and practice management (use of clinical judgment) interrelate when performing cost research for life care plans. Published standards of practice and consensus and majority statements serve as foundational, top-tier documents, from which practice management flows, representing the individualized approaches life care planners use to research and document costs. Life care planners use the foundational documents as guidance and rely on clinical judgment informed by their education, training, and experience (learning) along with a review of relevant resources and references, to select costing technique(s) appropriate to the items and services required to meet an evaluee’s needs within a life care plan.

Figure 2 represents two costing techniques, aggregated data and individual research, and highlights key considerations associated with the use of each approach. The considerations are defined as strengths and challenges related to the application of these techniques. Additional information regarding strengths and challenges is provided in Chapters 5, 6, and 7 and summarized in Tables 2 and 3.

The Costing Framework, as illustrated in Figure 2, may be used by life care planners to help select the appropriate techniques and sources for each item in a life care plan. Information has been provided in Chapter 1 to help life care planners determine whether a given technique or source is consistent with standards of practice and consensus statements. Clinical judgement is then applied to costing in each situation. This may include application of jurisdictional requirements impacting the work product. Considerations revealed in the data may further assist in the selection of appropriate techniques and sources, i.e. selection of a database that provides costs that are geographically specific and current, or selection of individual costing sources for specialized items in a life care plan.

Discussion

The purpose of this project was to create a Costing Framework to educate and guide life care planners regarding costing techniques currently used in the life care planning community. Since the first Life Care Planning Summit in 2000, costing has been an ongoing and evolving topic among life care planners, with 2017 Summit participants requesting more costing guidance through the development of a framework (Johnson et al., 2023). No such framework was created until this project was initiated in 2022. Through a review of foundational life care planning documents and relevant publications related to costing research as well as synthesis of results from the 2021 Costing Technique Survey and the 2022 Summit, the Costing Framework presented in this chapter was developed.

During the synthesis of findings, five consistent themes emerged from the survey and summit data: aggregated data, individual research, learning, practice management, and standards of practice / consensus and majority statements. Life care planners commonly reported the use of aggregated data and individual research costing techniques as reliable and reproducible, in alignment with established standards within the life care planning community.

In addition to following published guidelines, life care planners reported learning how to cost services and products through formal training programs, on-the-job experience, mentorship, or other non-formal training. Also, guidelines and learning techniques influenced life care planners’ development of practice management skills, including the application of individual clinical judgment and objectivity while using consistent methodologies to obtain costs according to jurisdictional requirements that may impact the work product. Examples of practice management were reported when life care planners selected specific percentiles, databases, codes, customary and reasonable (UCR), and geographically represented costs. Ninety-three percent of respondents reported identifying cost sources within their plans, while 85% reported using codes when researching medical, surgical, and diagnostic procedures. Furthermore, the majority of life care planners reported using multiple valid techniques to determine costs, with results expressed in various formats such as averages or ranges.

Two costing techniques, aggregated data and individual research, were reported as valid and reliable methods for obtaining geographically specific costs. Sixty-two percent of respondents reported using databases that contain synthesized data compiled from multiple sources and a larger sample. A majority also identified direct inquiries and individual research methods, such as telephone calls (77%) and email correspondence (72%) with specific providers and vendors, as valid approaches for determining costs in a specific geographic area. Aggregated data were also reported as accessible through books and software products. When using aggregated data, life care planners reported relying on paid subscription databases, fee-based data downloads, and free databases to determine costs. In addition to direct inquiries, individual research methods included review of medical bills, fee schedules, internet websites, and facility chargemasters. The use of these two costing techniques is consistent with prior life care planning research, including Neulicht et al. (2022), who reported that life care planners contacted local vendors (64%) and used national databases with geographic adjustment (59%).

Furthermore, the Costing Framework presents considerations related to the use of different costing techniques. Commonly reported strengths associated with aggregated data included validity, reliability, geographic specificity, consistency, statistical rigor, accessibility, and the availability of large data sets. Strengths associated with the individual research included the ability to obtain evaluee-specific costs, access costs that may not be available through other methods and differentiate among providers and specialties. Costs obtained through individual research were reported to be verifiable, valid, reliable, accurate, and geographically specific.

Challenges associated with the use of these costing techniques were also reported. When using aggregated data, some types of costs were reported to be unavailable, and the data was reported as not being specific to treating providers. Also, life care planners indicated that aggregated data may lack differentiation by provider specialty, and there may be a user learning curve. Challenges related to individual research included the time-intensive nature of the process and the potential of varied costs for the same service. Life care planners also reported difficulty obtaining information at times when conducting individual research and a smaller sample size.

Limitations

The Costing Framework is based on a 2021 Costing Technique Survey as well as 2022 Summit Top Hat responses and discussions data. Therefore, findings reflect experiences of participants who responded to the survey and/or participated in the 2022 Summit. While the number of respondents and representative demographics provide a meaningful sampling of the life care planning community, additional research with a larger sample of life care planners may further strengthen and expand these findings. Data were collected in 2021-2022, reflecting costing methods commonly used during that timeframe.

Conclusion

The Costing Framework Development Committee achieved their primary goal of developing a Costing Framework to support life care planners in defining and defending their costing methodologies within their individual practice settings. This goal was accomplished through the collaborative efforts of the Costing Framework working group and advisory committee. The framework is intended to be flexible, allowing life care planners to exercise clinical judgment in their cost research decisions. In addition to the material presented in this chapter, variables to be considered in cost-related decisions as well as circumstances in which those variables are relevant are addressed in Chapters 4, 5, 6, 7, and 8.

Costing remains a central issue in life care planning, and further research is recommended to address costs associated with emerging health interventions, specialized services, and the methods available to access and determine how to apply source data in life care plan costing. This Costing Framework is intended to evolve as the practice of life care planning advances. For example, price transparency federal rules and chargemasters were first initiated in 2021, but these topics were not reflected in the 2021 costing survey questions and were not a focus at the 2022 Summit because use of chargemasters and price transparency lists was limited at that time. Future research regarding use of chargemasters and price transparency lists in life care plan costing is recommended.

Additionally, research has also been suggested regarding sampling methodologies when conducting direct cost inquiries. Maniha and Watson (2019) proposed the use of the Area Cost Analysis Form as a structured data-gathering tool and Barros-Bailey et al. (2022) introduced an Attendant Care Survey Methodology (ACSM) to collect attendant care costs. However, further research is encouraged to identify more data-gathering tools for costing purposes. Findings from Chapter 7 indicate a need for additional education regarding percentiles obtained from multiple databases, which is beyond the scope of this project. A detailed discussion of percentile usage and interpretation was provided by Mertes and Reid (2024). Furthermore, investigation of costing techniques used by life care planners outside of the United States would contribute to the advancement of life care planning practice globally.